Have you ever wondered why, just as the calendar year begins to settle into its rhythm, India suddenly hits a financial reset button on 31 March? It might feel arbitrary at first glance, but there is actually a fascinating mix of history, law, and economic logic behind it. Let’s break it down in a way that feels less like a textbook and more like a conversation.

A Legacy from the Colonial Era

To understand India’s financial year, we need to rewind to the time of British rule.

The April to March financial year was not originally an Indian invention. It was inherited from the British administrative system. Back then, the British Empire aligned its fiscal practices across colonies for easier governance. India adopted this system, and even after independence in 1947, it stayed in place.

Why didn’t India change it immediately?

Because continuity matters, especially in something as complex as taxation and budgeting. Transitioning systems is not just about changing dates. It involves overhauling accounting frameworks, business cycles, and government processes.

The Legal Backbone

From a legal standpoint, the financial year in India is defined through statutes like the Income Tax Act, 1961 and various financial regulations.

Under Indian law:

- The term “previous year” refers to the financial year from 1 April to 31 March

- Taxes are assessed based on income earned during this period

This structure ensures:

- Uniformity in tax reporting

- Predictability for businesses and individuals

- Alignment with government budgeting cycles

Changing the financial year would require legislative amendments across multiple laws, not just a simple administrative tweak.

The Economic Logic: It’s About Timing

Now comes the more practical question. Why April to March specifically?

The answer lies in India’s economic structure, especially its historical dependence on agriculture.

1. Agricultural Cycle Alignment

India’s economy has long been tied to the monsoon and harvest cycles. By March:

- The rabi crop harvest is nearing completion

- The government has clearer visibility on agricultural output

This timing allows policymakers to:

- Estimate rural income levels

- Plan subsidies and expenditures more effectively

2. Better Budget Planning

The Union Budget is typically presented in early February. This gives:

- Time for parliamentary approval

- Departments to prepare for implementation from April

If the financial year began in January, budget approvals might clash with year end closing activities.

3. Business and Accounting Convenience

Most businesses benefit from:

- Closing accounts after the peak economic activity period

- Starting fresh books at the beginning of a new operational cycle

April serves as a natural clean slate for financial planning.

Why Not Switch to January to December?

This question comes up often, especially since many countries follow the calendar year.

India has actually explored this idea. Committees, including one led by economist Shankar Acharya, examined whether a January to December financial year might be better.

Pros of switching:

- Alignment with global financial systems

- Easier comparison of international data

But the challenges are significant:

- Massive transition costs for businesses

- Disruption in tax systems and reporting

- Misalignment with India’s agricultural and monsoon cycles

In short, the benefits do not clearly outweigh the complexity, at least not yet.

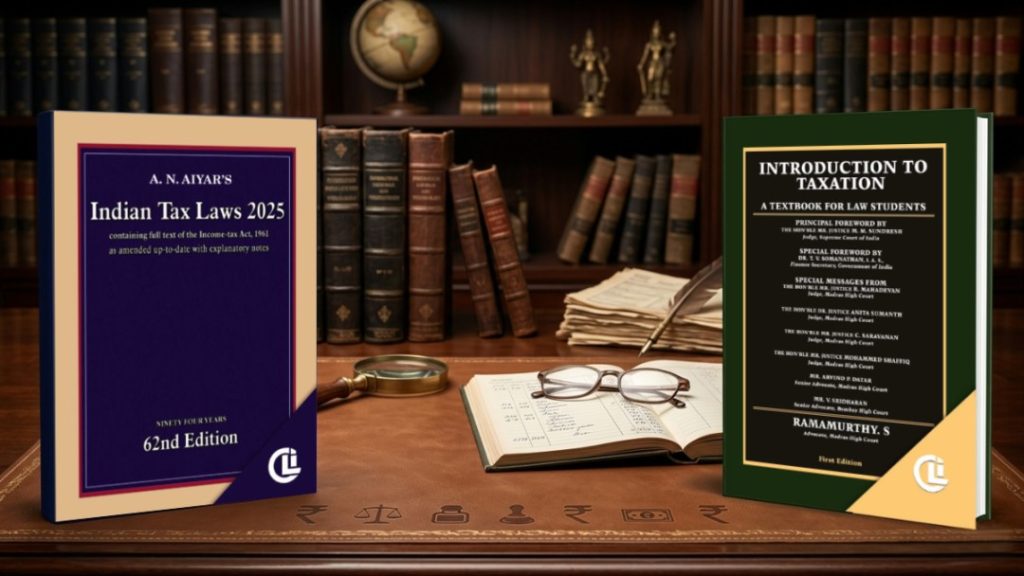

If you’d like to explore this topic in greater depth, you can refer to the following resource.

A.N. Aiyar’s Indian Tax Laws 2025

Introduction to Taxation: A Textbook for Law Students